Why do employees embezzle? How to protect your business

Feb. 6, 2019

This paid piece is sponsored by Eide Bailly LLP.

By Eric Hansen, CFE, CFI, Forensic Accounting Manager

It doesn’t happen in Sioux Falls! Not to our business! Our employees would never steal! Comments like these are not only incorrect but they also are commonly heard when Eide Bailly’s forensic team is brought in to investigate a possible embezzlement.

No one wants to believe their trusted employees would pocket money. But it happens here in Sioux Falls. And it occurs more than anyone would like to believe.

So what makes these fraudsters steal from their employer, and how can you prevent or detect fraud in your business?

The 4 “B”s

Our forensic team has years of experience learning why embezzlers steal. Forensic accountants have discovered employees generally embezzle for at least one of the four “B”s.

- Bills: Employees may embezzle because they are having financial difficulties and need money to pay their bills.

- Bets: Gambling addiction is a common reason employees steal funds so they can pay for their need to bet.

- Booze: Employees may have a drug, alcohol or other addiction that causes them to embezzle to pay for these habits.

- Bling: Living beyond one’s means or “keeping up with the Joneses” is another reason employees steal so they can pay for a lifestyle outside their current means.

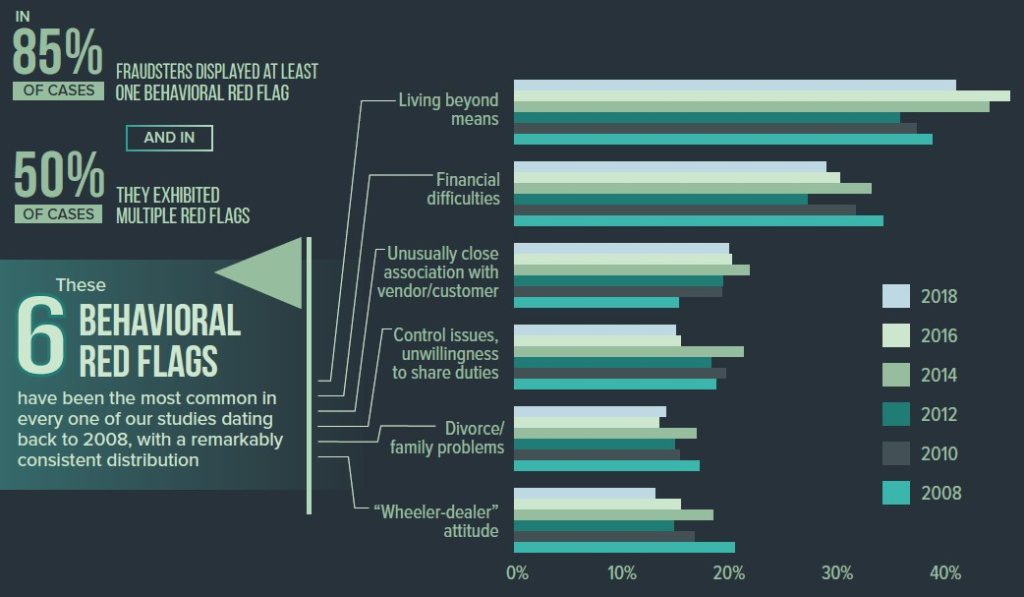

These signs, or red flags, let an employer know that an employee may be struggling and may need help. If you have an employee who is exhibiting some of these signs, it is important to examine the employee’s job duties and identify what risk/opportunity the employee may have to steal from the organization.

According to the 2018 Association of Certified Fraud Examiner’s Report to the Nations, other top red flags include:

- Employees who have unusually close relationships with vendors or customers.

- Employees who are unwilling to share their job duties and let other get involved with their work.

- Employees going through divorce or experiencing family problems.

- Employees who have a “wheeler-dealer” attitude.

It’s important for business owners to remember that when we are talking about fraudsters embezzling from a business, it’s not always money they are taking. It may be embezzlement in the form of inventory or payroll.

Example: Inventory theft

A past fraud investigation identified a scheme involving an employee theft of $950,000 worth of medical and office supplies over a four-year period. The employee was responsible for all duties involving inventory, from ordering to receiving and counting to recording. This employee stole these items from their employer, sold them online and used the funds for gambling.

The organization noticed the large inventory adjustments being taken for these items but believed it was a business problem, not a fraud problem, until they eventually retained us. After a thorough forensic accounting and computer forensic examination, this scheme was identified, documented and turned over to authorities for criminal prosecution and restitution.

Internal controls

Like many South Dakota businesses, there are not enough staff and resources to implement perfect internal controls to prevent all fraud from happening. That’s OK! Although a business may be unable to prevent fraud from occurring, the business should be able to detect fraud to minimize any losses.

Some common preventative internal controls include:

- Blank checks and company credits cards are stored in a locked drawer.

- Dual authorization methods are used for electronic bank transfers.

- Accounting and computer software has user restrictions that limit access to individuals.

- Inventory is locked with limited employee access.

- Employee background checks are performed.

The following detective controls can be helpful in identifying fraud:

- Bank reconciliations, including cancelled checks, are reviewed by someone independent of the accounts payable process.

- Mandatory vacations or cross-training/job rotations are required for staff.

- Inventory counts are done by someone other than the person ordering, receiving and recording inventory.

- Credit card statements are received and reconciled by someone who does not have access to a company credit card.

- Audit trail from an organization’s accounting system should be reviewed for unusual activity.

- Periodic surprise “audits” or request for invoices/supporting records should be performed by someone independent of those handling the day-to-day accounting for an organization.

To gain peace of mind about the security of your company, contact Eric Hansen at [email protected] or 605-367-6757. To learn more about how to avoid fraud, click here.